Azea Networks, upgrading submarine cables

May 2007

For some reason I've always been intrigued by

Azea Networks. I'm not sure why, maybe it's because of the market area they are involved with -submarine cable

upgrades - or maybe it's because they have a way of doing this at lower cost than the jaw-dropping amount of money it takes to lay a new cable.

For some reason I've always been intrigued by

Azea Networks. I'm not sure why, maybe it's because of the market area they are involved with -submarine cable

upgrades - or maybe it's because they have a way of doing this at lower cost than the jaw-dropping amount of money it takes to lay a new cable.

My interest was reawakened when I saw that Azea had recently attracted

a $20m investment -

Subsea network provider Azea secures $20M in more funding so I thought I would take the opportunity to write a post about them and catch up with Scott White, Azea's Founder and CEO.

My interest was reawakened when I saw that Azea had recently attracted

a $20m investment -

Subsea network provider Azea secures $20M in more funding so I thought I would take the opportunity to write a post about them and catch up with Scott White, Azea's Founder and CEO.

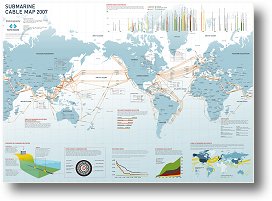

I think most of us have heard of submarine telecommunications cables as they are such a fundamental part of modern voice and data telecommunications. There are multiple cables straddling the world's oceans and if you would like to see the extent of the network then you can buy a definitive map from TeleGeography which shows the locations of over 120 cables.

(Picture credit:

C&W) The first cables were laid in the 19th century to interconnect telegraphic networks around the world following the

invention of the telegraph in 1837. What followed was a ceaseless decade-by-decade addition of new cables and their replacement as new services demanded better technology and higher bandwidths.

This continues to the current day.

(Picture credit:

C&W) The first cables were laid in the 19th century to interconnect telegraphic networks around the world following the

invention of the telegraph in 1837. What followed was a ceaseless decade-by-decade addition of new cables and their replacement as new services demanded better technology and higher bandwidths.

This continues to the current day.

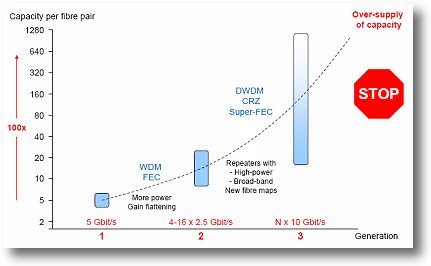

Early cables were electrical in nature but with the advent of optical fibers, they soon made the transition to optical technology. Initially they could only support a single channel, but with the development of Wave Division Multiplexing (WDM) technologies - covered in Making SDH, DWDM and packet friendly and optical amplifiers, the capacities available on submarine cables literally exploded to multiple 10Gbit/s in the late 1990s. This was driven by the then prevalent forecasts that the requirement for bandwidth would soar into the stratosphere over the next decade. Around 12billion Dollars was spent by existing telecommunications companies and a raft of start-ups financed by the venture capital community and all were hoping to make a significant return on their investments. All this new money fed significant research and development that really did move the state of the art from WDM through to Dense DWM (DWDM).

As a graph from Azea shows above, capacities on single submarine cables increased from 5Gbit/s through to Nx10Gbit/s over a number of technology generations delivered over a period of a decade.

And then came the melt down...

When the telecommunication market crashes in 2001, deployment of new cables was severely curtailed as there was over-capacity in the market leading to plummeting wholesale prices. Many of the new market entrants sadly went into receivership, many investors were burnt and the industry shrank to virtually only keeping lights on at night.

The renewed need for capacity

There is a clear analogy here with the co-location industry as covered in Colo crisis for the UK Internet and IT industry? which at the same time crashed in a similar way. The irony in both cases is that a five year period of non-investment has led to a market situation where there is severe under-capacity. All the sky-high forecasts that drove the 'bubble' are now coming to fruition leading to my opinion that the downturn will be seen retrospectively as a blip in the continuing growth of global data traffic.

In the same way that under-capacity is driving new commercial opportunities in the colo market, it's also leading to new opportunities in the submarine cable market. This is where Azea comes in to the picture.

Laying new submarine cables are phenomenally

expensive projects, so expensive that they were usually financed and owned by a consortium of interested carriers. These days carriers are reluctant to invest in such expensive projects that

are associated with such a long pay-back period. Interestingly, most telecommunications infrastructure investments were written off over 25-year periods but that has pretty much ceased over the

last few years with investors and shareholders chasing returns over much shorter periods such as three to five years.

Laying new submarine cables are phenomenally

expensive projects, so expensive that they were usually financed and owned by a consortium of interested carriers. These days carriers are reluctant to invest in such expensive projects that

are associated with such a long pay-back period. Interestingly, most telecommunications infrastructure investments were written off over 25-year periods but that has pretty much ceased over the

last few years with investors and shareholders chasing returns over much shorter periods such as three to five years.

In the last few years, much investment in R&D new cable technologies has slowed, particularly in the area of 40Gbit/s+ technologies. Strong competition for the few new cable laying opportunities has led to low prices on 10Gbit/s technologies.

When existing capacity starts to run out on a particular submarine path there are several ways that this issue could be addressed.

-

Leave alone: In other words, just ignore the problem and find a work around by shipping traffic on other paths. This could create long-term problems.

-

Build a new system: Very expensive, long lead time to deployment and a long-term commitment. Not an investment profile liked by 21st century carrier Boards and shareholders.

-

Lease capacity: If capacity is availably - and it's a big 'if' - then it could be made availably quickly but it comes at high cost in these days of under supply.

-

Upgrade capacity: This is a viable alternative that could provide capacity quite quickly at 'modest' cost.

It is in this last alternative that Azea networks plays by providing a methodology and a technology that can be used to hot-upgrade an existing cable without the need to take it off-line.

There is one caveat on this ability and that is only submarine cables that use optical amplifiers can be upgraded. Those using regenerators cannot. The reason for this is that a regenerator converts modulated light streams back to an electrical signals prior to regenerating them on another segment of cable thus channels and data rates are hard-embedded in the system and cannot be changed.

Upgrade alternatives

Dark fibre: As with terrestrial optical systems, lighting a dark fibre or unused fibre to add new capacity is a straightforward exercise with little impact on other lit fibres. Unfortunately, there are not too many dark fibres on submarine cables!

Overlay upgrade: An overlay upgrade can be used in parallel with existing services and works by inserting new wavelengths using an optical coupler that run together with existing WDM channels. Care is needed to avoid disrupting existing traffic. This approach does represent a compromise as it would not achieve the capacity that could be obtained by replacing WDM equipment in totality, but it does represent a cost effective solution.

Retrofit upgrade: A hybrid upgrade uses a mix of optical couplers and a replacement of equipment. This is more challenging as it could affect existing equipment warranties. This is most common for older generation systems where the existing terminal is obsolete and uses too much spectrum inefficiently.

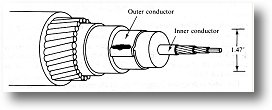

When upgrading a live cable a high level of

planning is required beforehand if disruption to existing services are to be avoided. Each cable incorporates a number of optical amplifiers as shown in the picture above. Each amplifier

introduces noise which accumulates along the cable. Also each amplifier and fibre segment introduce distortion which again accumulates along the cable length. These effects limit the data rate

that can be achieved on a particular cable and the number, if any, new channels that can be inserted.

When upgrading a live cable a high level of

planning is required beforehand if disruption to existing services are to be avoided. Each cable incorporates a number of optical amplifiers as shown in the picture above. Each amplifier

introduces noise which accumulates along the cable. Also each amplifier and fibre segment introduce distortion which again accumulates along the cable length. These effects limit the data rate

that can be achieved on a particular cable and the number, if any, new channels that can be inserted.

The upgrade process consists of the following steps:

-

Adding a coupler, checking existing traffic and measuring the existing performance.

-

Connect new equipment

-

Check existing traffic and new traffic.

An nice animation of these activities can be found here and an information-full presentation entitled Upgrades: Theory and Practice is worth studying.

Roundup

In 2006 Azea announced that it has successfully completed Phase 1 of an upgrade to Segment I of the Southern Cross Cable Network (SCCN) and been selected for Phase 2 of the upgrade. Since then they have completed additional projects and are working on others as I write.

According to Scott White, Azea's CEO, "Although there is only one customer in the public domain, we now have a deployment track record that covers all the upgrade scenarios across different generations of cable system technology and different upgrade methodologies. We are confident that on any given cable system we can offer the best upgrade solution � the most capacity, at the lowest price, deployed in the shortest time. In addition, because we are 100% focussed on upgrades we are often seen as being more independent than the larger submarine system suppliers who also push the more expensive option of building entirely new systems. However, we do not expect to win all upgrade opportunities as there is sometimes a strong allegiance to a particular vendor in some carriers."

Scott confirmed my view that there has been a "huge pick up in industry optimism, especially in the submarine communications sector with a big uptake in both upgrades and new system builds". Moreover, "as a small company, the recent investment really helps provide the financial credibility we require to deal with some of the world's biggest carriers and we now have sufficient financial resources to see us through to profitability".

Submarine cables are a key element in the infrastructure that lies behind the Internet and private Wide Area Networks (WANs) and it's great to hear that the industry is recovering and beginning to deploy the bandwidth capacities we all need in our day to day use of networks.